Biofuels in Aviation

Overview

Aviation is one of the strongest growing transport sectors and this trend will continue. Biggest and fast-growing air passenger markets are the USA, China and India. In 2019, the total number of passengers travelling by air in the EU amounted to 1,034 million. An increasing traffic volume of about 3% annually is expected. However, due to the Covid-19 pandemic, which resulted in a dramatical decrease of passenger flights in 2020, future development is less predictable.

Commercial Aviation Fuel (CAF)

Commercial aviation fuel is a hydrocarbon, almost exclusively obtained from the kerosene fraction of crude oil. Two types of fuels are used in commercial aviation: Jet-A and Jet A-1. Fuel specifications for aviation fuels are very stringent.

According to Fuels Europe the demand for CAF in the EU amounted to 62.8 million t in 2018. All of this CAF had fossil origin, according to Bioenergy Europe.

Sustainable Aviation Fuels (SAF)

For aviation, advanced liquid biofuels are the only low-CO2 option for substituting kerosene, since a high specific energy content is required. Gaseous biofuels and electrification are challenging for air transportation, especially for long distance flights. Advanced biofuels for aviation should use sustainably produced feedstocks to produce a fuel that can be considered as substitute for commercial aviation fuel, while not consuming valuable food, land and water resources.

Globally, a number of airlines have signed biofuel offtake agreements, fifteen airports provide aviation biofuels on a regular basis and more than 250,000 commercial flights have flown on SAF blends. In the EU the annual production capacity of pure SAF amounted to 1,000 t from 2015 to 2017 and increased to 7,000 t in 2018, according to EUROSTAT. Examples for European airlines, with long-term contracts for SAF are Lufthansa and KLM.

SAF Production pathways

Globally, various sustainable feedstocks and conversion technologies for production of biofuels for aviation are currently being developed by research organisations, airlines, fuel producers and aircraft manufactures. In the short term, HEFA appears to be the most promising alternative to supply significant amounts of biofuel for aviation. In the medium term, the most promising alternative is drop-in FT-fuels. Testing of biofuels is crucial to determine suitability for aviation. In the testing process, which aims to maintain the highest standards in safety, biofuels must undergo dozens of experiments in the laboratory, on the ground and in the air.

ASTM-certified biofuels represent no technical or safety problem in flights. Currently, the following biofuel production pathways are approved by the standard:

- Alcohol to Jet Synthetic Paraffinic Kerosene (ATJ-SPK, up to 30% blend): This biofuel is created from isobutanol which is derived from feedstocks such as sugar, corn or wood. The alcohol is dehydrated to an olefinic gas, oligomerized, hydrogenated and fractionated.

- Synthesized iso-paraffins (SIP, up to 10% blend): This biofuel is based on sugars that are converted to a pure paraffin molecule using an advanced fermentation.

- Hydro-processed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK, up to 50% blend): This biofuel is made from vegetable oils and animal fats, which are deoxygenated and hydroprocessed.

- Fischer-Tropsch Synthetic Paraffinic Kerosene (FT-SPK, up to 50% blend): This biofuel is based on the gasification of biomass, followed by Fischer-Tropsch synthesis.

- Fischer-Tropsch Synthetic Kerosene with Aromatics (FT-SPK with aromatics): Some alkylated benzenes of non-petroleum origin are added to the FT-SPK.

- HC-HEFA-SPK – lipids from Botryococcus braunii algae, up to 10% blend

- Catalytic hydrothermolysis jet fuel (CHJ), using triglycerides, such as soybean, jatropha, camelina or carinata oil, up to 50% blend

- Co-processing of lipids, up to 5% blend

- Fischer-Tropsch biocrude as feedstock for co-processing in refineries, up to 5% blend

Several additional pathways are currently under review by ASTM. Examples are: Synthetic kerosene/synthetic aromatic kerosene (Shell, Virent), HEFA with improved cold flow rates – HEFA+ (Boeing) and pyrolysis from lignocellulosic feedstocks.

Future perspectives for biofuels in air transport

Aviation is responsible for about 2% of CO2 emission induced by humans and about 12% CO2 emissions in the transport sector. Since 2012, flights entering the EU are required to pay for CO2 emissions due to the EU Emission Trading System (ETS). Sustainable aviation fuels are currently being discussed as an important way to reduce aviation's greenhouse gas emissions. The aviation sector has voluntarily committed itself to CO2-neutral growth from 2020 onwards, and alongside efficiency-boosting measures, sustainable aviation fuels are a key building block.

The estimated current production of sustainable aviation fuels is around 0.05% of current aviation fuel consumption. Some first producers of sustainable aviation fuels worldwide are e.g. World Energy in Paramount, USA, Neste in Porvoo, Finland, Gevo in Silsbee, USA, Total in La Mede, France and Fulcrum in Sierra, USA. The largest share is HEFA-SPK based on fats and oils. The commissioning of additional plants is announced for 2022, which will increase production capacity tenfold.

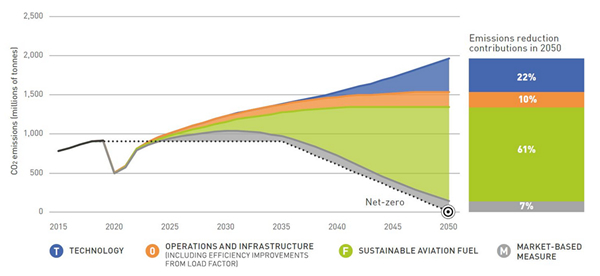

The Waypoint 2050 report, published by the Air Transport Action Group (ATAG) in 2021, includes three scenarios. The figure below shows the respective share of technology improvements, efficiency improvements and SAF utilization on GHG emission reductions, with a focus on technology improvements (Scenario 1).

Legal and political framework for sustainable aviation fuels

So far, there is no obligation for the aviation sector to use SAF, and EU emission targets alone only lead to minor increase in SAF production. On 14th July 2021, the European Commission published a proposal for a directive as part of the fit-for-55 package, which provides for binding requirements. According to this proposal, aviation fuel suppliers in all EU member states should provide 2% SAF in 2025. The mandatory share will increase in 5-year steps to 63% SAF in 2050. The details of the directive are still under discussion between the Commission, Council and Parliament.

There is policy at EU level for the production and use of biofuels in the aviation sector and several initiatives have been established:

- The International Civil Aviation Organization (ICAO) has developed a Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). ICAO set the ambitious target of 50% GHG emission reduction until 2050 (compared to 2005). CORSIA aims to implement that each airline has to compensate its emissions, above a baseline. A first pilot phase has started in 2021 and is planned until 2023, followed by a voluntary phase from 2024-2016 and, finally by a mandatory phase from 2027-2035. This scheme aims for offsetting 80% of the air traffic growth after 2020.

- Coordination of RED II and CORSIA will be crucial for the aviation sector. Key components of both policies are minimum sustainability criteria and how these are ensured and certified. Mandates for SAF were already announced by some Member States. SAF volumes produced must be registered, they have to be accounted under both, RED II and CORSIA. CO2 savings calculation need particular attention, since there are differences in national emission counting. It must be ensured that the transposition of these two schemes in MS legislation takes this into account to avoid carbon counting conflicts. However, GHG emission reduction requirements are quite different (10% for CORSIA, 65% for RED II).

- The High-Level Group on Aviation Research sets ambitious goals including a 75 % reduction in CO2 emissions and a 90 % reduction in NOX emissions per passenger kilometre in 2050. The same document also claims that Europe should be established as a centre of excellence on sustainable alternative fuels, based on a strong European energy policy.

- The International Air Transport Association is committed to achieve carbon-neutral growth starting 2020 and a 50 % overall CO2 emissions reduction by 2050

- In 2011, the European Commission, in coordination with airlines and biofuel producers, launched the “European Advanced Biofuels Flightpath” initiative as a roadmap to produce 2 million tonnes of SAF per year until 2020. The Flightpath initiative supports and promotes production, storage and distribution of SAF. However, the production target was not fulfilled. As biggest obstacles, economic, policy and market related issues, were identified.

- Other projects and initiatives, such as “Bioport Holland”[1] or IATA[1] also aim for supporting SAF production in Europe. E.g. IATA introduced three emission targets for the whole aviation industry. One is to cut net emission in half by 2050 compared to 2005.

|

Drivers and Opportunities |

Barriers and Challenges |

|

|